This article should not be construed as financial advice. You should work with your own financial professional to determine the strategies that are right for you and your financial situation.

Compound Interest: Einstein’s 8th Wonder of the World

Albert Einstein once said, “Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it.”

Einstein is best known for revolutionizing the way we understand space and time. With compound interest, time is on your side. And you don’t have to be Einstein to understand why. Here’s how it works:

What Is Compound Interest and Why Does It Matter?

There are two main types of interest:

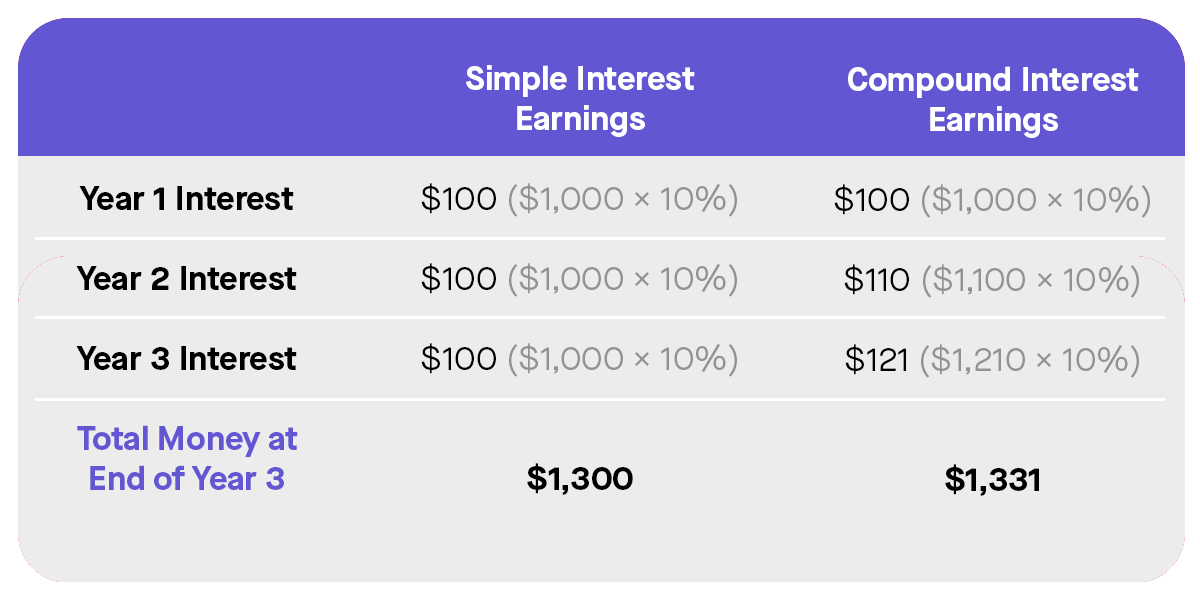

- Simple interest pays interest on your initial investment. For instance, if you put $1,000 in an investment that pays 10% in simple interest, you’ll earn $100 each year you leave your money invested.

- Compound interest pays interest on your initial investment plus interest on the interest you earn. If you place the same $1,000 in an investment that pays 10% in compound interest, you will earn $100 each year you leave your money invested plus an additional amount from interest on interest. For instance, you earn $100 of interest during your first year and reinvest that $100 — so in the second year, you earn 10% of $1,100 for a total of $110 of interest.

With a $1,000 investment that pays 10% in interest, a yearly breakdown of your return would look like this:

Understanding the difference between simple and compound interest can make all the difference in securing long-term returns from your investments. If you’re trying to grow your wealth over a long period of time, you may want to look for ways to leverage compound interest in your investment strategy.

For investments lasting less than one year, simple interest is more convenient. But in other cases, assuming constant and equal interest rates, you’ll almost always come out ahead by choosing compound interest accounts.

‘He who understands it, earns it; he who doesn’t, pays it’

It pays to be on the earning side of the equation. Banks pay you pretty low interest rates (less than 0.05% if you’re like most of America) while taking your money and loaning it out to other people at a much higher rate. They are likely reinvesting the interest they earn and compounding their earnings, while you are stuck with the same flat (or falling) rate for keeping your money with them. By putting money in a savings account, you’re financing their loans and their profits.

Investments That Compound Easily

Bonds

When you purchase a bond, you provide a loan to a company or public entity. They're set up to give you regular interest payments on the amount you’ve loaned, as long as the loanee doesn’t default on payments. Regular interest payments for bonds are similar to the dividends you might receive on stock investments and can be monthly, quarterly, or annual depending on the terms of the bond.

Some companies like SMBX have bonds designed to pay out monthly, so you can quickly reinvest in your next bond — this way, your investment compounds easily. SMBX offers Small Business Bonds™ so you can invest in local small businesses that matter to you. By reinvesting your payments, including both interest and principal, your investments can start compounding.

Stocks

There are many types of stocks. Some pay dividends, while others are considered growth stocks, which generally don’t pay dividends. Income stocks are set up to pay out dividends on a regular schedule.

By reinvesting dividends and using funds to purchase additional shares of stock, investors can generate compounding returns — the shares purchased with dividends create additional dividends when the next payment is made.

Dividends, paid either quarterly or annually, are not always guaranteed. Companies are free to change the dividend depending on current market conditions or internal company plans. Sometimes, during periods of high capital reserves, companies might pay out special dividends. These instances are niche cases, and you shouldn’t expect them to happen in the future.

Rental Properties

Rental properties can provide regular income in the form of rent. If the rent is higher than your monthly mortgage payment and associated expenses, you’ll have extra funds that can be reinvested in other rental properties or investments to earn compound returns.

If you own enough rental properties that bring positive cash flow, you’ll eventually be able to buy additional rental properties without needing to invest additional capital.

Investments That Don’t Compound Easily

Bank Accounts

Bank accounts. They’re useful for paying bills and collecting money, but not so great in terms of investing. With interest rates below 0.05%, even if you leave your money alone, it’ll lose value because of inflation, which is currently around 1.7%. (Remember that soda you could buy for 50 cents as a kid that now costs $1.25?)

But bank accounts are the simplest example of compounding interest — either a savings account or an interest-bearing checking account. These types of bank accounts provide low returns in exchange for easy access to funds.

Bank accounts usually pay interest based on compounding interest rules. Each month, the bank calculates the average amount of money in the account, including any interest received in the previous month, and pays interest on that amount. The interest compounds over time. But with such low interest rates, don’t expect any meaningful earnings. (0.05%, really?)

Startup Equity

It might be exciting to invest in a startup — a shiny new company with enthusiastic owners who are driven to make the company succeed. But don’t let the early motivation get you. Startups are a gamble, to say the least, and at best you’ll have to be patient. It may take years to see a return on your investment (if you see one at all), which doesn’t leave room for annual compounding.

Fine Art

Whether you think fine art resembles a toddler’s drawing or you have a more discerning eye, fine art may be an appealing alternative investment. However, owning a piece of art won’t provide any income during the lifetime of your investment. Unless you put the piece on display and expect donations, you won’t receive any regular payments or similar earnings. Without regular interest payments throughout the time you own the piece, it will be impossible to reinvest or earn from interest.

Growth Stocks

Growth stocks are labeled as such because the company reinvests its earnings to fuel growth instead of making dividend payments to shareholders. Growth stocks generally don’t pay dividends.

Because all the reinvestment value is wrapped up in the stock’s value, you won’t be able to reinvest your portion of the company’s earnings, making it harder to compound your investment.

Precious Metals

If your investment strategy involves precious metals, you won’t earn interest or dividends on your associated holdings. Unless you’ve been blessed (or cursed!) with a literal Midas touch, precious metals won’t actually grow in quantity.

Though precious metals can serve as a hedge against inflation, they don’t create any income while they’re in your possession — as with fine art pieces, you won’t be able to reinvest your earnings or accrue interest from regular payments.

What Type of Investment Is Most Valuable?

All other things being equal, an account that pays compound interest compared to one that pays simple interest will have greater returns in the long run. However, if you’re trying to decide on interest rates for other investments, the winner is less clear.

When making investment decisions, you might try looking for investments that provide regular income that can be reinvested or used to purchase new assets. These investments can let you recoup your initial funds, diversify your portfolio, and maximize your returns.

Before making any investment, you should determine:

- Your tolerance for risk

- The returns you’re looking for

- The period of time you’re willing to have your funds be inaccessible

Each of these criteria will play a significant role in determining which investments are right for you.